Editor’s Note: I came across this fascinating piece about natural wine in China. It traces the arc of natural wine from its boom in Shanghai to the nationwide downturn to its current recalibration, linking the rise and fall to distinctly China-specific factors. It also asks the bigger question: what is the future of natural wine in China? Throughout, sharp observations from Zita Hu, a wine importer and co-owner of TonAri wine bistro in Shanghai, with some real insight.

The article below was originally written in Chinese by Zita Hu for Sommelier Press (待酒师画报), published June 30, 2026. Translated by Rachel Gouk.

Shanghai’s Natural Wine Bistro SOiF Closes

Shanghai’s well-known natural wine bistro SOiF quietly shut its doors at the end of June 2026.

SOiF was never just an ordinary wine bar. It opened on Wuding Road in September 2020, led by some of the Vinism founders, and quickly became the standard-bearer for Shanghai’s natural wine movement. Food and wine writer Rachel Gouk once described it as “one of the few bars leading the revival of Shanghai’s wine bar scene,” and Star Wine List named it a must-visit wine bar in the city.

In under six years, natural wine went from championing a revival to a dimmed existence. Once a byword for what was cool and trending, it has since faded into the background. These days, whether at small neighborhood bars or online shops, natural wine bottles are no longer flying off the shelves, and mentions of natural wine on social media have grown noticeably scarcer.

Is SOiF’s closure a full stop, or just a comma?

A Hard Truth: Market Pressure Is Shrinking the Scene

Shanghai is one of the birthplaces of China’s natural wine trend — Vinism’s opening in 2017 is widely regarded as the starting point of the movement nationwide, and bars like SOiF quickly followed and took off. Around 2020, searching “natural wine” (自然酒) on Dianping yielded more than 83,000 results in Shanghai alone, far outpacing the 26,000 results for “craft beer.” The wave of enthusiasm quickly spread to Guangzhou, Shenzhen, Chongqing, Chengdu and other cities, where natural wine accounted for more than half of offerings at many new bars.

But the momentum didn’t last. During the pandemic, roughly 5,700 bars closed across China, according to Zhiyan Consulting (智研咨询数据). Wine bars, already a niche category, were hit especially hard. In Shanghai, the Vinism brand was sold off, Ambra shut down, and RAC was sold to a coffee giant [M Stand]. It seemed that people were no longer buying into “natural wine”.

Chengdu tells a similarly grim story. Leading wine bars like La La Land and Wine Universe (宇宙酒馆) closed, and a host of copycat bars struggled to survive. Stephen Yang, founder of Hō Wine Bar & Eatery, put it plainly: Then, wine revenue dropped to around 70-75%, further slipping to around 60% currently. Unstable foot traffic combined with high operating costs make things increasingly difficult in the current climate where consumer spending is downgrading.

Beijing, Guangzhou, and Shenzhen likewise went from a boom of new openings to a Darwinian shakedown. Early natural-wine bistros that relied on a formula of “atmosphere + natural wine + food” have largely withdrawn from the market, lacking stable repeat customers and consistent quality.

The Global Data: Is Natural Wine Really in Decline?

Some argue that the cooling of natural wine in China is simply part of a broader downturn in the global wine market. But the data tells a different story.

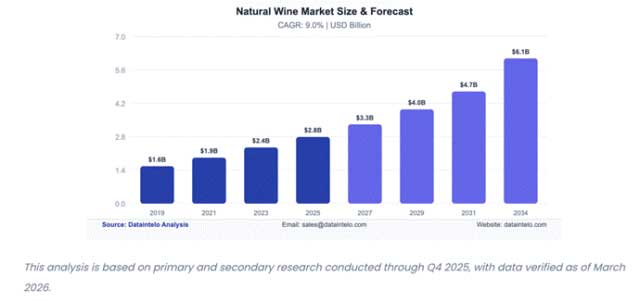

According to a report by Dataintelo, the global natural wine market was valued at roughly $2.8 billion in 2025 and is projected to reach $6.1 billion by 2034, a compound annual growth rate (CAGR) of 9.0%. The organic wine market — which overlaps heavily with natural wine — was already worth $12.9 billion globally in 2024 (InsightAce Analytic), and is expected to grow to $42.3 billion by 2034, at a CAGR of roughly 12.7%.

In Europe in 2025, France alone had 2,655 natural wine venues and Italy had 1,623; Paris accounted for 599 of them, up 36% from 2021. Growth in North America was stronger still: natural wine sales in the US had a CAGR of 14.2% between 2022 and 2025, while retail SKUs grew 38% over the same period. Even in Asia, where the base is smaller, the CAGR from 2026 to 2034 is projected to reach 12.8% — though that growth is driven mainly by markets like Japan, South Korea, and Australia. China’s sluggish performance, by contrast, is actually dragging down the Asia-Pacific numbers.

So, Where Did It Go Wrong?

Let’s revisit the natural wine boom that swept China between 2017 and 2020: capital poured in, and social media packaged natural wine as a kind of attitude and symbol — a prop for a certain identity turned into content fodder. People weren’t drinking wine; they were projecting a persona.

As the concept took off, countless copycats followed and bars multiplied rapidly. But the market skipped over all the groundwork needed to sustain real, lasting consumption. Consumers never had the time to understand what natural wine was. The category had already been distorted — its value determined not by what was in the glass, but by how Instagrammable it was.

Capital, hungry for quick returns, along with no shortage of so-called experts, had little patience for actually explaining to consumers what natural wine meant. Bandwagon-jumping KOLs led people to believe that oxidation, brett [brettanomyces, aka yeastiness], and volatile acidity were the signature flavors of natural wine. On the supply side, inferior products were passed off as premium, and prices inflated. Once capital had harvested its crop, and consumers were unwilling to spend again, the hype quickly receded — it was just unsustainable.

In contrast, natural wine overseas is nothing new. Natural wine only entered mainstream markets overseas after decades of accumulated winemaking philosophy, sommelier training, and consumer education. Natural wine — which pushes back against excessive intervention and emphasizes an honest expression of grape and terroir — fits neatly with what mature markets are genuinely looking for: low intervention, transparency, sustainability. Its growth abroad, against the tide of the overall wine market, is built on consumers’ understanding of terroir and authenticity, not on brands exploiting a trendy label.

To quote Simon Woolf, author of Amber Revolution: “natural” is not a style, a taste or a smell. It doesn’t mean a cloudy, cidery-smelling liquid brimming with volatility, neither does it represent a star-bright, manicured creation that feels polished to perfection. Paradoxically, it could be either of those things, or neither. It’s not a religion, a creed or a caste — at least it shouldn’t be. [Wine Scholar Guide]

In mature markets, consumers choose natural wine not for its “funky” aesthetic or as a rebellious statement. Its value lies in the terroir and the grape itself, supported by a “right to know” mindset of opinionated consumption. This confidence allows natural wine to grow against the global wine market’s downward trend.

China’s problem is that it skipped past understanding the methodology and went straight to consuming the label and postures. And once “natural” shifts from being a method to being a symbol, from a choice to a stance, from a drink to an identity, it’s unlikely to go the distance.

So, Has Natural Wine Really Gone Cold in China?

The author of this piece [Zita Hu] believes that natural wine’s so-called “cooldown” is merely the fading of capital-driven hype and the influencer filter wearing off — a return to rationality.

According to a Nielsen report, 30% of young people in China still say they enjoy natural, additive-free alcoholic drinks, up 12 percentage points from five years ago. More of China’s Gen Y and Gen Z consumers are growing immune to older generations’ lecturing and to “influencer wines.” They’re no longer willing to blindly chase “famous château, high-scoring, internet-famous” bottles — instead, they buy only once they genuinely understand, have tasted, and actually like something.

From within the industry, what’s happening now looks like a sorting-out process. Natural wine no longer shows up as a slogan-ready category label — a marketing term that once worked well but has since taken on a slightly negative connotation. On the other hand, natural wines are appearing more and more frequently on the wine lists of high-end restaurants.

Operators who lack real understanding and expertise are gradually being weeded out. The importers, restaurants, and retailers that remain are being more selective about wineries and are exploring suitable ways to present them across different settings. Meanwhile, consumer knowledge is growing too. Those who moved from chasing photo ops to genuinely loving the wine will keep choosing natural wine in the right context. They no place value in how quirky a label looks or how photogenic a bottle is — they ask only one question: is this wine right for me?

At this stage, natural wine no longer stands in opposition to commercial wine. It no longer needs to prove what it stands for; instead, it returns to the market as a sub-category of wine choices. Perhaps this is precisely a sign of a maturing market.

Natural wine may never become the mainstream choice in China’s wine market. But precisely for that reason, it has a rare resilience: it allows for nuances, accommodates imperfection, and continually reminds us that wine does not have only one standard answer. And maybe that’s closer to what drinking wine is really about.

Read the original article in Chinese here (WeChat).